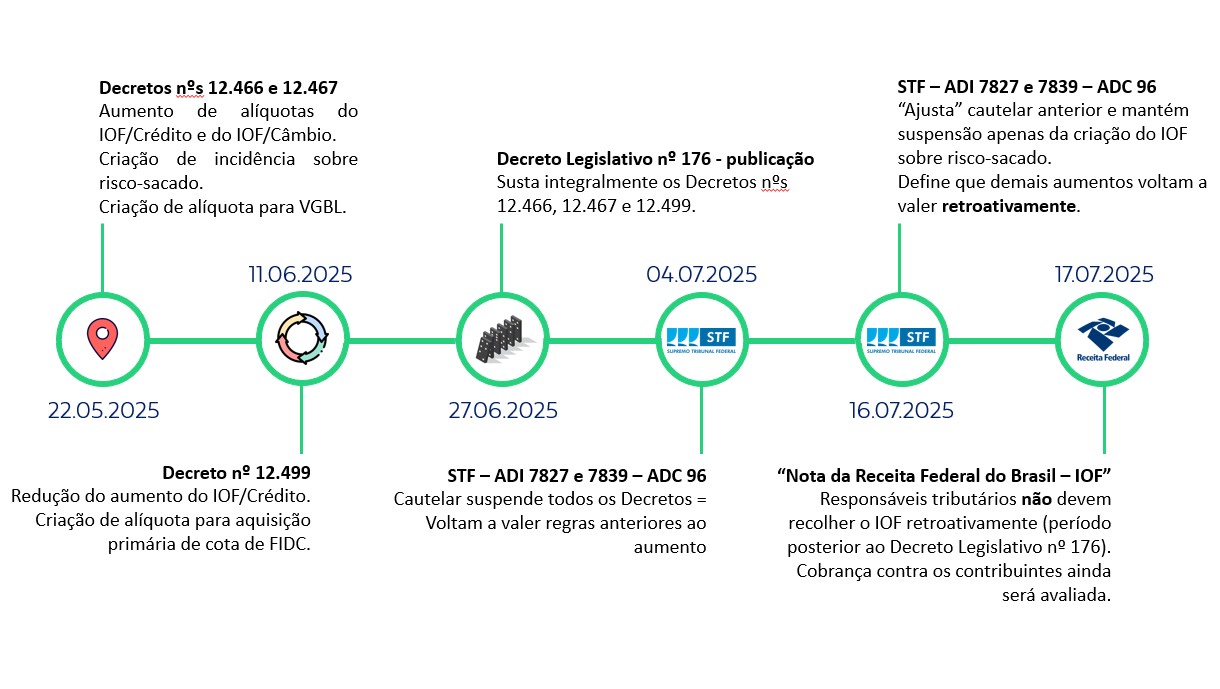

The Federal Government's initiative to increase the Tax on Financial Transactions (Imposto sobre Operações Financeiras – IOF) rates on various transactions underwent significant developments since our prior advisory (link), as may be seen in the following timeline:

The single-justice ruling (decisão monocrática) issued by Justice Alexandre de Moraes on July 16, 2025 created enormous legal uncertainty, as it would permit the collection of IOF pursuant to the guidelines of Decrees Nos. 12,466, 12,467, and 12,499 with respect to transactions that occurred during the period in which such Decrees had already been stayed by Legislative Decree No. 176 and were suspended by the preliminary injunction (cautelar) initially granted by the Federal Supreme Court (Supremo Tribunal Federal – STF) itself.

The single-justice ruling (decisão monocrática) issued by Justice Alexandre de Moraes on July 16, 2025 created enormous legal uncertainty, as it would permit the collection of IOF pursuant to the guidelines of Decrees Nos. 12,466, 12,467, and 12,499 with respect to transactions that occurred during the period in which such Decrees had already been stayed by Legislative Decree No. 176 and were suspended by the preliminary injunction (cautelar) initially granted by the Federal Supreme Court (Supremo Tribunal Federal – STF) itself.

In other words, by virtue of that ruling, taxpayers and withholding agents who simply complied with the legislation that was actually in force during that period could be subject to retroactive collection of the tax and, potentially, of late-payment surcharges.

Fortunately, the Brazilian Federal Revenue Service (Receita Federal do Brasil) adopted a reasonable position and waived the risk of IOF collection against withholding agents, who, strictly speaking, could not have acted otherwise.

Nevertheless, the possibility of retroactive collection from taxpayers maintains this state of uncertainty, which will only be resolved if the full bench (Plenário) of the STF, upon reviewing the confirmation of the preliminary injunction, overturns the retroactive effect of the July 16, 2025 ruling, or reinstates the suspension of Decrees Nos. 12,466, 12,467, and 12,499.

Even if that does not occur, late-payment surcharges should at a minimum be excluded from any potential collection, in compliance with art. 100, sole paragraph, of the National Tax Code (Código Tributário Nacional – CTN).

The Tax team at FreitasLeite is available to provide further clarification.