On May 22, 2025, the Federal Government published Decree No. 12,466/2025, increasing the Tax on Financial Transactions (Imposto sobre Operações Financeiras – IOF) rates on various credit, foreign exchange, and insurance transactions. In view of the negative market reaction to the measure, Decree No. 12,467/2025 was already published on May 23, 2025, partially reversing the rate increases.

Set forth below are the main changes introduced.

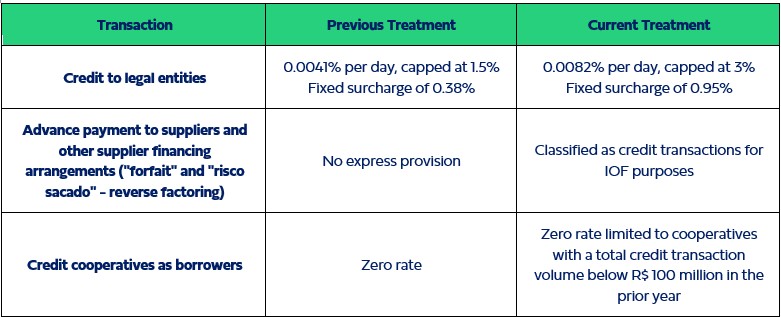

1. IOF on Credit Transactions

The IOF rate on credit transactions was increased in the following circumstances:

Questions may arise regarding the assimilation of transactions involving the advance payment of suppliers and other supplier financing arrangements ("forfait" and "risco sacado" — reverse factoring) to credit transactions for purposes of IOF incidence by means of a Decree, given that Decrees may not create new taxable events, not even for a regulatory tax such as the IOF. Accordingly, such assimilation is contingent upon the classification of these transactions within taxable events already set forth in a statute (Lei).

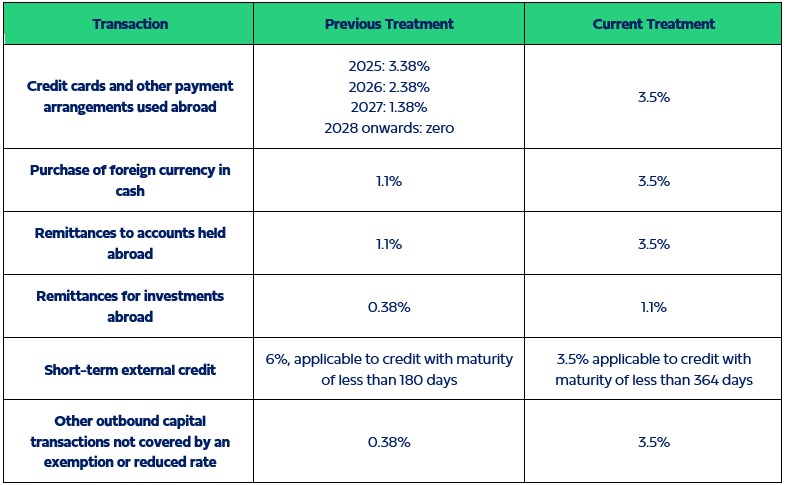

2. IOF on Foreign Exchange Transactions

2. IOF on Foreign Exchange Transactions

The main changes in the incidence of IOF on foreign exchange transactions may be summarized as set forth in the table below:

The Brazilian Federal Revenue Service (Receita Federal) may further regulate the incidence of IOF on remittances for investments abroad, which may clarify, for example, the tax authority's position on the application of this rule to remittances made for the capitalization of foreign companies.

Remittances by investment funds: initially, outbound remittances made by investment funds were also to be subject to a rate of 3.5%, but the Federal Government reversed course and such transactions remain subject to a zero rate.

We note that the new rates mark a departure from the commitment to align with OECD standards, which had been adopted in 2022 and aimed at the gradual reduction of IOF on foreign exchange transactions to zero by 2029, at which point all transactions would be subject to a zero rate.

The Federal Government also introduced the incidence of IOF on contributions to life insurance plans with survival coverage (cobertura por sobrevivência), which particularly affects VGBL plans (Vida Gerador de Benefício Livre).

As a result of the measure, contributions exceeding R$ 50,000.00 in a given month will be subject to taxation at a rate of 5%

4. Effective Date

The new rates took effect as of May 23, 2025, except with respect to "forfait" and "risco sacado" transactions, which will be subject to the new rates as of June 1, 2025.

5. Closing Remarks

In addition to the challenges raised above, the IOF rate increase at a time when the Federal Government is seeking new revenue to rebalance the public accounts will reignite discussions on the constitutionality of using this tax for fiscal purposes, or, at a minimum, on the need for such revenue-raising measures to comply with the principles of legality and non-retroactivity (anterioridade).

The Tax team at FreitasLeite is available to provide further clarification.