On March 18, 2025, the Federal Government submitted to Congress Bill No. 1,087/2025 ("Bill"), which proposes the taxation of profits and dividends distributed by Brazilian companies in certain circumstances, and establishes a minimum income tax for individuals, levied on income exceeding a specified threshold, designated as the Minimum Personal Income Tax (Imposto de Renda das Pessoas Fisicas Minimo - "IRPFM").

This measure is proposed as a counterpart to the reduction to zero of income tax for taxpayers with taxable income of up to R$ 60,000 per year (R$ 5,000 per month).

Set forth below are the main aspects of the IRPFM Bill, which is still subject to review by Congress.

1. Overview

Under the Bill, individuals with annual income exceeding R$ 600,000 (six hundred thousand reais) will be subject to the IRPFM, the rate of which may reach up to 10% for annual income exceeding R$ 1,200,000.

Almost all of the taxpayer's income sources are taken into account for this threshold, with certain exclusions detailed in item 2 below. As a result, certain income previously exempt, in particular profits and dividends, will become subject to IRPFM.

2. Taxable Base

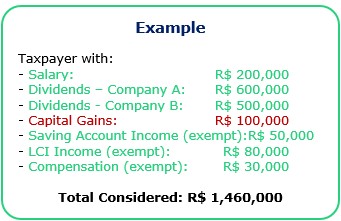

For purposes of calculating the R$ 600,000 threshold, all of the taxpayer's income shall be considered, even if exempt or subject to exclusive withholding at source, with the exception of the following:

- Capital gains (except those arising from stock exchange transactions).

- Accumulated income (Rendimentos Recebidos Acumuladamente - RRA) taxed exclusively at source.

- Inheritances and donations in advance of legal succession (adiantamento de legitima).

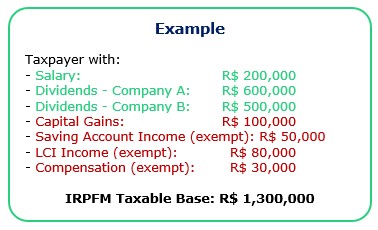

Once the initial threshold has been calculated, the taxpayer may deduct the following amounts from the IRPFM taxable base:

- Savings account income.

- Securities (titulos e valores mobiliarios) that are exempt or subject to a zero rate, except for income from shares and other equity interests.

- Compensation for workplace accidents, property damage, or moral damages, except for loss of profits (lucros cessantes).

- Retirement or disability benefits arising from workplace accidents, or received by holders of certain serious diseases, and pensions received by holders of such diseases.

3. IRPFM Rate and Computation

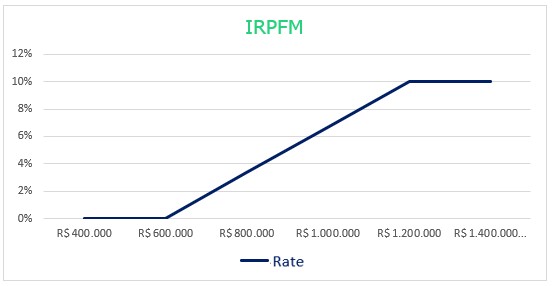

The IRPFM rate shall vary according to the total income considered in the calculation of the R$ 600,000 threshold and shall increase linearly for income from that threshold up to R$ 1,200,000. Above that level, the rate shall be 10%:

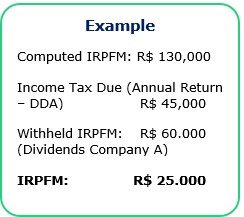

In the example used, considering total income of R$ 1,460,000, the IRPFM rate would be 10%. This rate would apply to a taxable base of R$ 1,300,000, resulting in a computed IRPFM of R$ 130,000.

To determine the IRPFM effectively due, the taxpayer may deduct:

- IRPF due on taxable income (e.g., salaries and rental income, among others).

- IRPF withheld exclusively at source on income that has been included in the IRPFM taxable base (e.g., withholding tax on financial investments).

- IRPF computed on offshore income (e.g., profits from controlled entities abroad or income from financial investments abroad).

- IRPF definitively paid with respect to income included in the IRPFM taxable base and not taken into account in the items above.

- IRPFM withheld at source on profits and dividends, as detailed in item 4 below.

- The amount of the dividend credit (redutor) applicable to profits and dividends, which will be detailed in item 5 below.

If the amount computed after the above deductions is negative, the IRPFM shall be zero.

The computed IRPFM shall be added to the IRPF balance payable or refundable as determined in the annual tax return (declaracao de ajuste anual - DAA).

4. IRPFM Withholding on Dividends

The Bill provides that dividends paid or credited by a company, in an amount exceeding R$ 50,000 in a given month to a single taxpayer, shall be subject to IRPFM withholding at a rate of 10% on the total amount of such dividends.

The withheld IRPFM is treated as a tax advance and shall be deducted from the IRPFM due at the end of the year.

5. IRPFM Dividend Credit (Redutor)

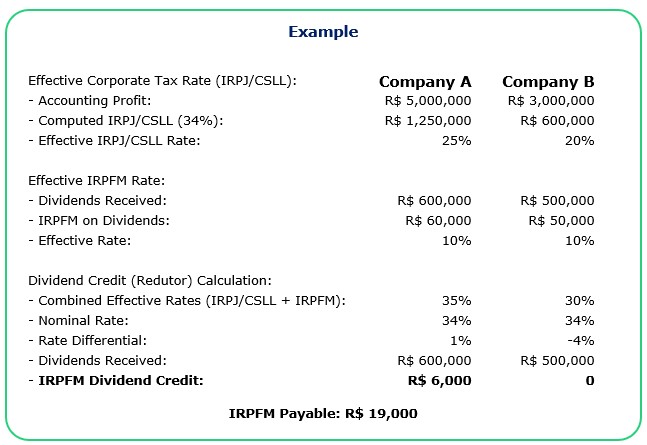

Given that the companies distributing profits and dividends are already subject to income taxation by means of the IRPJ/CSLL, the Bill seeks to minimize the impact of the IRPFM on such income through a tax credit mechanism (redutor).

The credit will be calculated so that the effective IRPJ/CSLL rate on the company's profits, plus the effective IRPFM rate on such dividends, does not exceed the nominal IRPJ/CSLL rate applicable to each dividend-paying company.

It is important to note that the nominal IRPJ/CSLL rates are as follows:

- 34%, for companies in general;

- 40%, for insurance companies and certain financial institutions, such as foreign exchange and securities dealers and brokers;

- 45%, for banks of any kind.

It should be noted that the effective IRPJ/CSLL rate will be based on the company's accounting profit, not on taxable profit. This effective rate may be calculated based on the consolidated financial statements of the dividend-paying company. There is also a provision for an optional simplified mechanism for the calculation of the effective rate by companies subject to the computation of IRPJ/CSLL under the Assumed Profit (Lucro Presumido) regime.

The grant of the credit is conditioned upon the submission of financial statements to the tax authority, in the form to be approved by regulation.

6. Dividends Remitted Abroad

6. Dividends Remitted Abroad

The Bill provides that dividends remitted abroad will become subject to income tax withholding at a rate of 10%.

Where the sum of the effective IRPJ/CSLL rate of the dividend-paying company and the 10% rate exceeds the nominal IRPJ/CSLL rate applicable to the company, the non-resident beneficiary may claim a tax credit within 360 days. Such credit shall be calculated in a manner similar to the dividend credit (redutor) described in item 5 above.

The Bill does not clarify whether such credit may be refunded and/or offset against withholding tax to be applied on future dividend distributions.

7. Points of Attention

We highlight the following points of attention regarding the Bill:

- Only donations in advance of legal succession (adiantamento de legitima) are excluded from the IRPFM taxable base, which may result in income tax applying to other types of donations.

- It is unclear whether the net gains from stock exchange transactions included in the IRPFM taxable base take into account the carryforward of losses from prior periods.

- The computation of the effective rate for purposes of applying the IRPFM dividend credit may give rise to distortions, because: (i) it is based on the entity's accounting profit, which may include revenues temporarily excluded for purposes of computing taxable profit; (ii) it does not take into account the possible carryforward of tax losses by the company, which would reduce the effective rate; and (iii) dividends received may originate from profits computed in years prior to the year of their actual distribution.

- Minority shareholders may face difficulty in obtaining the IRPFM dividend credit, as they may have limited access to the financial statements of the dividend-paying company.

The computation of the credit based on consolidated financial statements may give rise to distortions, including as a result of investments in affiliated entities, which are not included in the consolidation.

8. Legislative Process and Effective Date

The Bill is still subject to review by Congress, which may reject or amend it.

The Federal Government requested priority (urgencia) in the processing of the Bill, meaning that its progress through Congress should be expedited.

If the Bill is approved, even with amendments, the IRPFM may only be collected on income earned as of the year following that of its publication as a Law.

This means that, if approved in 2025, its rules will take effect as of 2026.