On December 26, 2025, Complementary Law No. 224/2025 ("LC No. 224/2025") was published, introducing several relevant amendments to the tax legislation, in particular (i) the reduction of various tax benefits, (ii) the increase in deemed profit margins for the Assumed Profit (Lucro Presumido) regime; (iii) the increase in the Social Contribution on Net Income (CSLL) rate applicable to certain financial institutions; and (iv) the increase in the rate applicable to Interest on Net Equity (JCP).

Set forth below are the most relevant aspects of the new legislation.

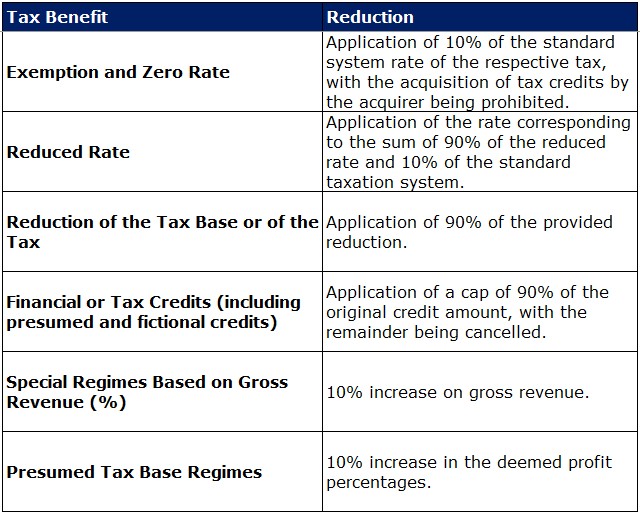

1. Reduction of Tax Benefits

LC No. 224/2025 establishes cumulative reductions in benefits applicable to federal taxes — PIS, COFINS, IRPJ, CSLL, II, IPI, and Employer Social Security Contributions, as set forth in the table below:

The amendments do not apply to:

The amendments do not apply to:

- Constitutional tax immunities;

- Benefits applicable to the Manaus Free Trade Zone and free trade areas;

- Zero rates on the National Basic Food Basket (and equivalent under LC No. 214/2025);

- Time-limited benefits with an already fulfilled onerous condition, as provided in projects approved through December 31, 2025;

- Benefits for non-profit organizations (OSCIP and OS Laws);

- Taxpayers subject to the Ad Rem rate (fuel and tobacco sectors);

- Simples Nacional and other special or simplified regimes for Micro and Small Enterprises;

- Tax benefits whose granting legislation provides for a global quantitative cap, subject to prior administrative authorization for use of the benefit;

- Prouni;

- Minha Casa, Minha Vida program;

- Tax offsets for radio and television broadcasters in connection with free electoral airtime;

- CPRB reductions set forth in arts. 7 through 10 of Law No. 12,546/2011; and

- Benefits for the industrial policy of the IT and semiconductor sectors.

The reduction of tax benefits was regulated by Decree No. 12,808/2025, published on December 30, 2025.

2. Increase in Taxation under the Assumed Profit Regime

As of LC No. 224/2025, taxpayers opting to compute IRPJ and CSLL under the Assumed Profit (Lucro Presumido) system will be subject to increased taxation:

- Annual Gross Revenue up to R$ 5 million: current deemed profit margin maintained;

- Portion of Annual Gross Revenue exceeding R$ 5 million: 10% increase in the applicable deemed profit percentages.

As a result, taxpayers subject to the 32% deemed profit margin (services in general), for example, will be subject to a margin of 35.2%.

In the quarterly regime, the R$ 5 million threshold shall be adjusted proportionally.

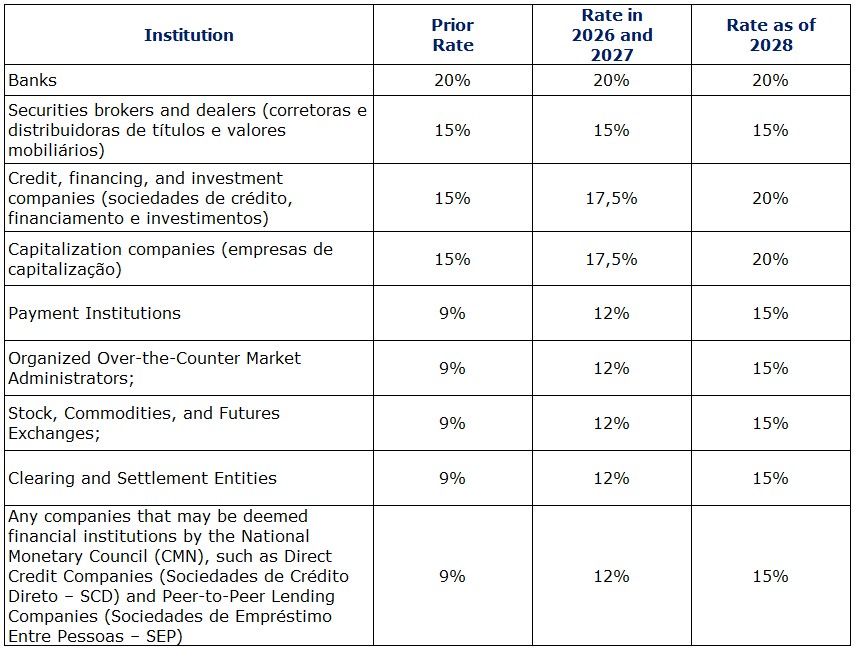

3. CSLL Rate Increase for Financial and Payment Institutions

LC No. 224/2025 permanently fixed the CSLL rate applicable to Banks at 20% and increased the rates for payment institutions and various financial institutions. For certain entities, the nominal rate increase may reach 6% by 2028.

Under the terms of the rule, the new rates shall take effect as of April 1, 2026.

Under the terms of the rule, the new rates shall take effect as of April 1, 2026.

The constitutionality of applying this increase during the course of 2026 may be challenged with respect to companies computing taxable income under the annual actual profit (Lucro Real) regime, given that taxes with complex taxable events (such as CSLL) must be subject to the legislation in force at the beginning of the occurrence of the respective taxable event (January 1, under the annual computation regime), as established by the Federal Supreme Court's case law.

4.Increase in IRRF on JCP Payments

JCP payments shall now be subject to withholding tax (IRRF) at a rate of 17.5%, instead of the prior 15%.

The deductibility of JCP in the computation of the actual profit of the paying company has been maintained.

5. Other Amendments: Extension of Tax Liability in the Context of Fixed-Odds Betting (Bets)

LC No. 224/2025 expands the entities solidarily liable for the collection of taxes levied on the exploitation of fixed-odds betting, expressly including:

- Financial and Payment Institutions, if, after notification by the authorities, they fail to adopt restrictive measures against unauthorized operators; and

- Advertising and public relations companies that broadcast advertisements for irregular operators.

For further information regarding LC No. 224/2025, the Tax team at FreitasLeite is available to assist.