On January 14, 2026, Complementary Law No. 227/2026 ("LC No. 227/2026") was published, introducing relevant amendments to the national tax legislation, particularly in the context of the Tax Reform.

Set forth below are the most relevant aspects of the new legislation with respect to the following taxes:

- ITCMD: Tax on Transfer Causa Mortis and Donations, levied by the States and the Federal District

-

ITBI: Tax on Onerous Real Estate Transfer, levied by Municipalities

1. Changes to ITCMD

LC No. 227/2026 established general rules regarding the ITCMD, which must be observed by the legislation of all States and the Federal District.

The enactment of these national guidelines, in addition to promoting alignment among state laws, addresses a longstanding legislative gap that had led to the declaration of unconstitutionality of ITCMD assessments in situations involving assets or persons located abroad.

It should be noted that, although general rules have been established, they do not have immediate applicability. Each State must enact its own legislation to regulate the guidelines set forth in LC No. 227/2026.

1.1. Mandatory Progressivity

In line with the provisions of Constitutional Amendment No. 132/2023, ITCMD rates shall be mandatorily progressive based on the value of the inheritance or donation.

Each State may define the progressivity of its rates, subject to the following parameters:

- Maximum rate of 8%, as set by the Federal Senate.

- Graduated application of rates (each bracket shall apply to the portion of the taxable base exceeding the threshold of the preceding bracket).

New state laws instituting progressivity shall observe the non-retroactivity principle, taking effect only from the year following that of their publication.

1.2. Valuation of Equity Interests

The valuation of equity interests for purposes of donation or succession shall observe the following criteria:

- Listed Shares or Quotas: if actively traded during the preceding 90 days, the closing price on the day before the valuation date shall be used.

- Unlisted Shares or Quotas (or without an active market): application of a technically sound methodology for the pricing of equity interests, subject to a minimum floor equivalent to the market value of the assets comprising the adjusted net equity, plus the market value of goodwill.

State legislation shall regulate the pricing methodologies applicable to unlisted equity interests.

The application of these criteria may result in a significant increase in the ITCMD taxable base, particularly in States that currently allow the use of book net equity value as the taxable base.

1.3. Successive Donations

In the case of successive donations between the same parties, all transfers carried out within a period to be determined by each state law shall be taken into account.

With each new donation, the taxable base and the tax amount shall be recalculated according to the progressive rates, with previously paid ITCMD being credited.

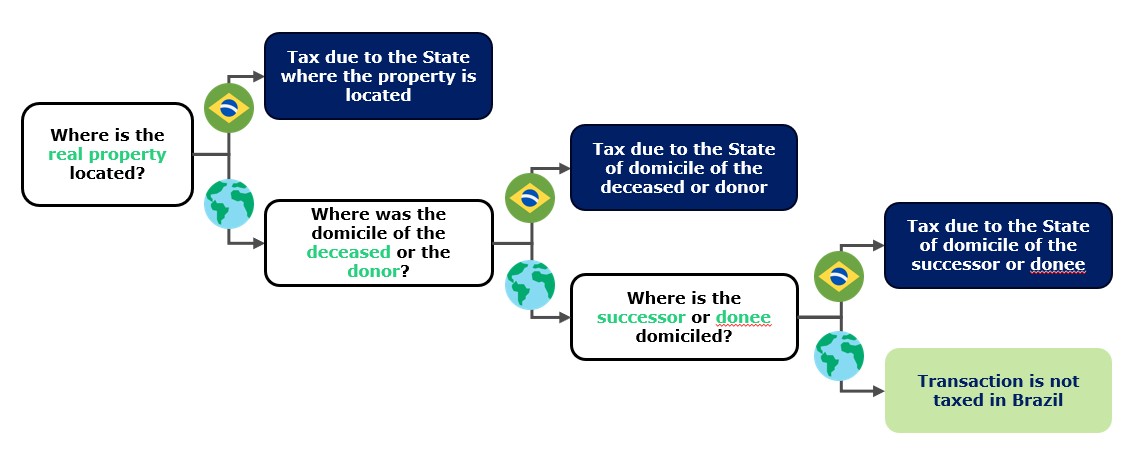

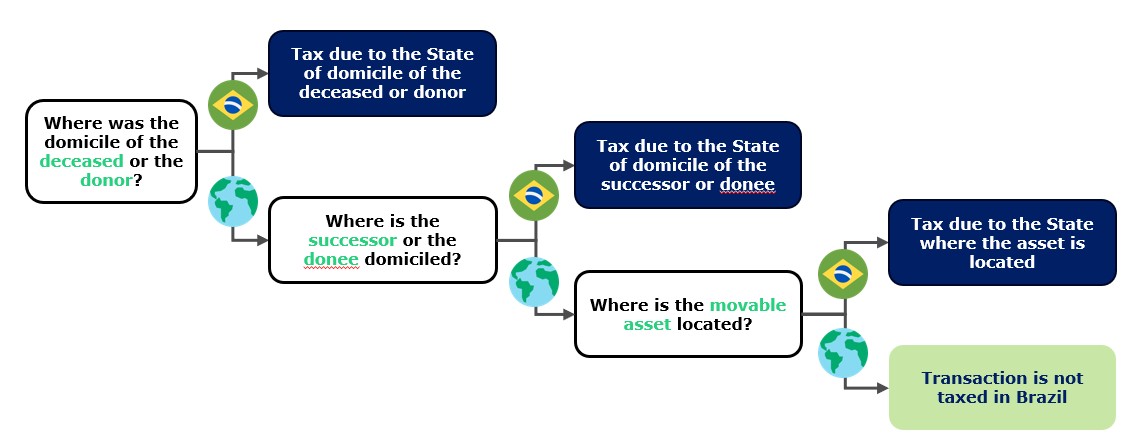

1.4. Competent State for Tax Assessment

As noted above, one of the primary objectives of LC No. 227/2026 was to establish national rules defining the competence of the States to tax situations involving a connection with foreign jurisdictions.

For this purpose, the States’ taxing competence was defined according to the nature of the transferred asset (real property or personal property), as illustrated in the flowcharts below.

- Real property

- Personal property

Furthermore, any new State law that begins to tax situations in which collection under prior legislation had been found unconstitutional by the STF shall only take effect from the year following its publication, subject to a minimum advance notice period of 90 days.

Accordingly, there remains a period during which certain situations will not be subject to ITCMD.

1.5. Trusts

The Complementary Law introduces specific rules for the transfer of assets in the context of trusts and similar arrangements, filling a gap that had long generated legal uncertainty on the subject.

The new rules clarify that the taxable event occurs at the moment of the transfer of ownership of the assets, subject to the following:

- If the transfer occurs while the settlor is still alive, it shall be treated as a donation; and

- If the transfer occurs as a result of the settlor's death, it shall be treated as a causa mortis

- The creation of an irrevocable trust in which the beneficiary is not the settlor itself is deemed a donation and shall be taxed at the time of the trust's creation

1.6. Usufruct

With respect to usufruct, the rule provides as follows:

- The taxable event is deemed to occur at the time of the creation of the usufruct.

- No tax shall be levied upon the extinguishment of the usufruct that results in the consolidation of full ownership in the settlor of the usufruct itself.

It is noted that the Complementary Law did not regulate the donation with reserved usufruct followed by the consolidation of ownership in the bare owner. Such situations may be regulated by the States, which may extend judicial disputes on the subject.

2. Amendments to ITBI

ITBI underwent targeted amendments through changes to provisions of the National Tax Code (CTN).

In particular, the new rule details criteria for the assessment of the market value of real estate by Municipalities, which may take into account:

- Analysis of prices prevailing in the real estate market;

- Information provided by financial institutions and registry services;

- Location, typology, intended use, area, and other characteristics; and

Other technical parameters customarily used in real estate valuation.

The text approved by Congress provided that payment of ITBI before registration at the Real Estate Registry (RGI) would be optional for the taxpayer, with municipalities able to establish reduced rates for early payment.

This rule sought to address a controversy still pending final adjudication by the STF regarding whether ITBI may be collected prior to the registration of the transfer at the RGI.

However, the President of the Republic vetoed this provision at the request of the National Mayors' Front

(Frente Nacional de Prefeitos), leaving the controversy unresolved.

For further information regarding LC No. 227/2026, the Tax and Wealth Planning teams at FreitasLeite are available to assist.